Project Work

As part of the DEFINE (Dynamic Ecosystem-FINance-Economy) team I develop country-specific ecological stock-flow consistent (SFC) macrofinancial models, combining the DEFINE approach with country-specific empirical modelling. I am currently developing models for Albania, in collaboration with the Bank of Albania, and the Philippines, with the Bangko Sentral ng Pilipinas, and extending the UK model, DEFINE-UK (see Completed).

Each model is individually developed to reflect the unique macroeconomic, financial and ecological context of the country being modelled.

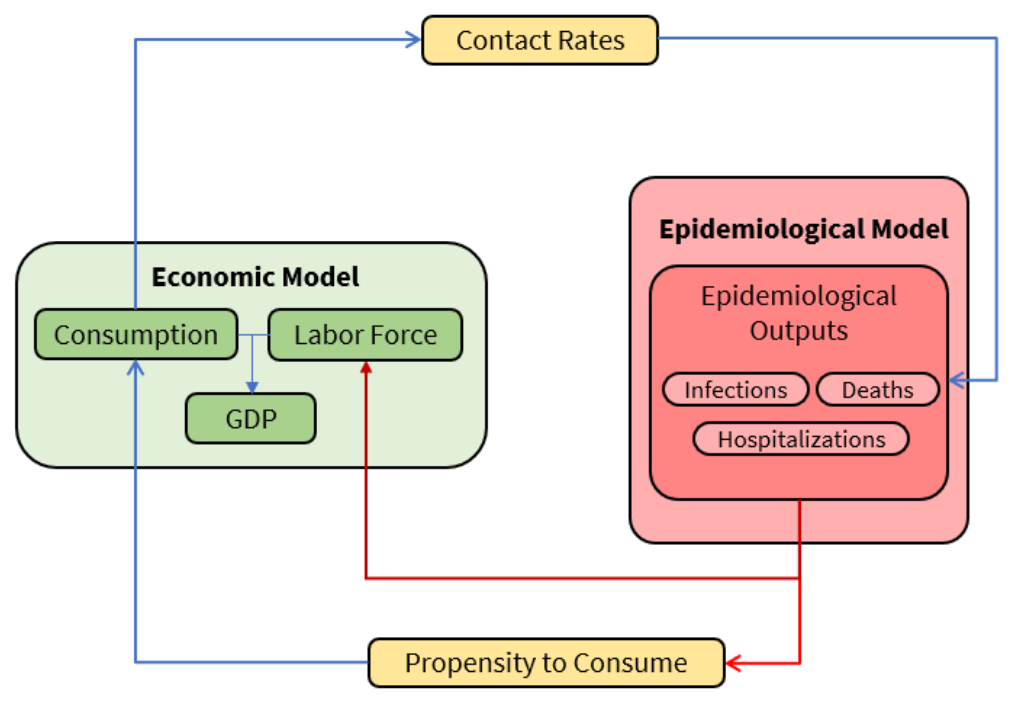

With the Jameel Institute at Imperial College London, alongside Ateneo de Manila University, I am contributing to the development of an integrated epidemiological-economic model that couples a compartmental epidemiological model with a stock-flow consistent (SFC) macroeconomic model in a single dynamical framework, parametrised for the Philippines.

The models are linked by two-way feedbacks (below): epidemiological outputs (infections, hospitalisations and deaths) reduce the population's propensity to consume and the available labour force, lowering consumption and GDP; in turn, changes in consumption and work alter contact rates and feed back into transmission. This lets the model explore the trade-off between infections and GDP loss under different behavioural responses.

Assessing Climate Policies in the UK: A Macrofinancial Modelling Approach

Completed PhD in Economics, SOAS University of London

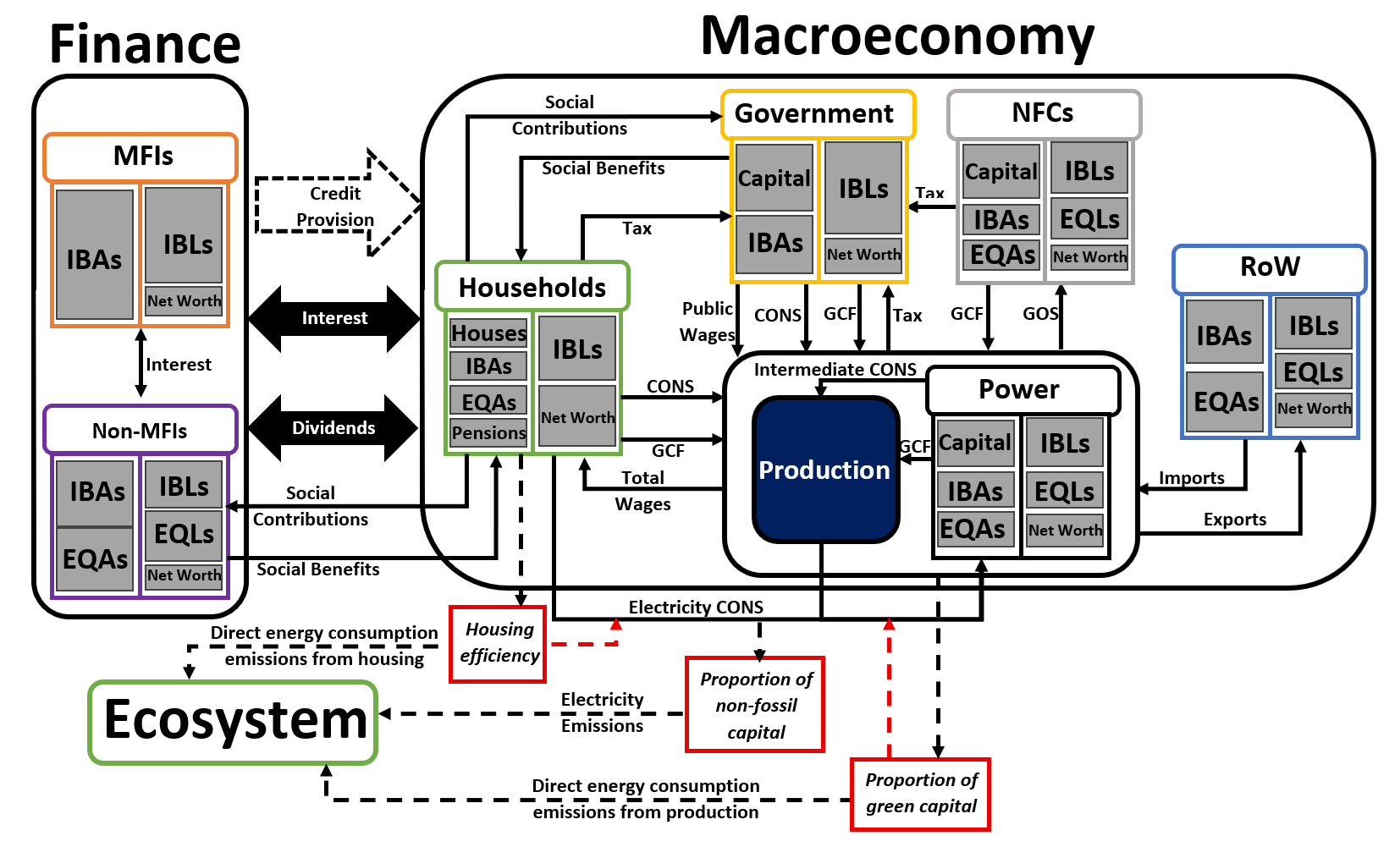

My PhD thesis developed DEFINE-UK V1.0, an ecological stock-flow consistent macrofinancial model of the UK, and used it to assess the macroeconomic, financial and ecological effects of UK climate policy mixes. The model is now being extended (see Ongoing).

The figure below summarises the structure of DEFINE-UK V1.0.

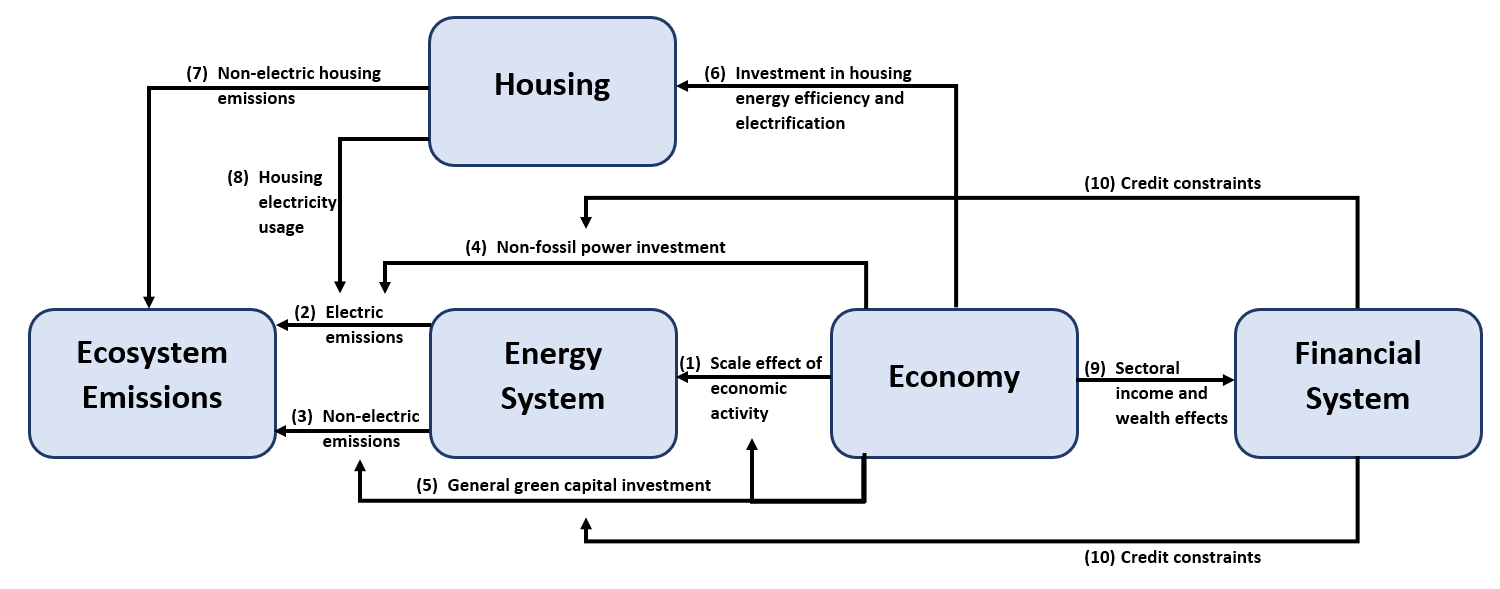

The key channels which integrate the macroeconomic, financial and ecological systems are shown below:

The channels are:

- The scale effect of economic activity: Representing how energy use is directly related to economic activity in the model. All else being equal, if there is more economic activity, then energy use will increase.

- The scale effect of energy use on electric emissions: Increased energy use leads to an increase in electricity use and emissions from electricity generation.

- The scale effect of energy use on non-electric emissions: Increased energy use leads to an increase in non-electric energy use and emissions from non-electric energy generation.

- Non-fossil power investment: Reduces the emissions from electricity generation by building non-fossil fuel based electricity generation capital.

- General green investment: This investment broadly captures investment in green capital, such as energy efficient buildings, electric appliances, and energy efficient machinery. This increases the stock of green capital relative to conventional capital. This in turn leads to a moderate reduction in the intensity of emissions from the use of non-fossil fuel energy, energy intensity and an increase in the electricity share of energy use. All effects together serve to dampen channels (1)–(3).

- Investment in energy efficiency and home electrification: This includes investment in housing energy efficiency and electrification improvements.

- Non-electric housing emissions: Housing emissions are not driven by economic activity but are instead primarily impacted by the quality of the housing stock with better energy efficiency and electrification of houses reducing these emissions.

- Housing electricity usage: With home improvements leading to greater electrification of homes this will increase electric emissions unless it is combined with an expansion of non-fossil power capital. Nevertheless, the net impact on emissions of these efficiency improvements is likely to be an overall reduction in emissions.

- The effects of sectoral income and wealth: Will affect the sectors' debt-service ratios while also directly affecting the financial position of banks and other financial corporations. These effects will impact the perceived credit-worthiness of these sectors.

- Credit constraints: Based on the perceived creditworthiness of the sector carrying out investments, banks will ration the availability of credit. This will constrain all types of investment in the model, including green investments.